Articles March 21, 2023

Healthcare Trends 2023: Technology Modernization Drives Improved Outcomes

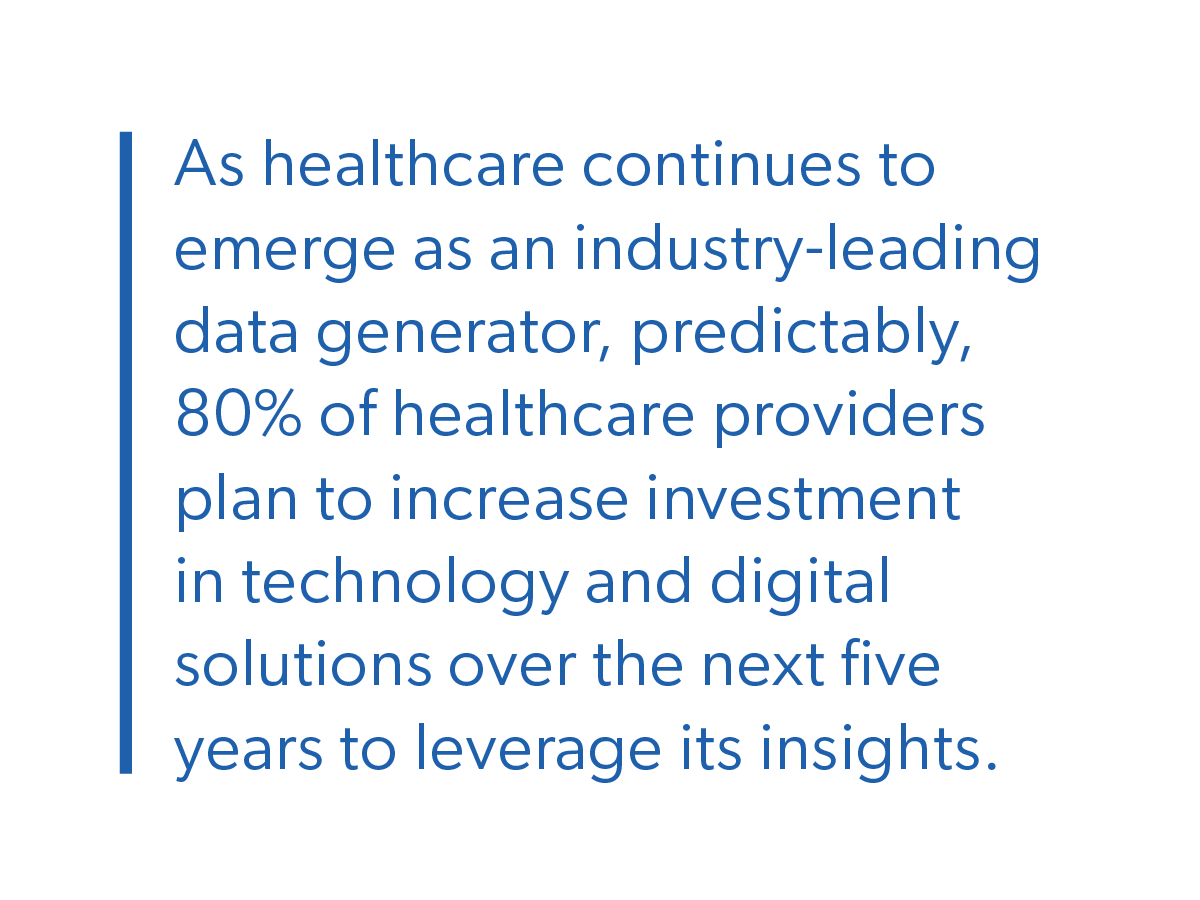

What else can be accomplished? Where do we go next?

Download the 2023 Healthcare Trends Report

Download

Jason Leonard

Principal, Healthcare and Public Services Industry Lead

Leading our Healthcare and Public Services portfolios, Jason has 15+ years of experience driving growth and client satisfaction. He specializes in integrated digital solutions to improve customer experiences and drive operational excellence. In healthcare, he focuses on actionable data solutions, AI acceleration, cloud adoption, and end-to-end product development to enhance patient outcomes. In public services, he helps modernize legacy systems, enhance citizen engagement, and optimize data strategies to streamline public services. A former CapTech client himself, Jason is passionate about achieving extraordinary stakeholder results.

Adam Hofheimer

Principal, Public Services

With 20+ years of technical expertise and visionary leadership, Adam has been instrumental in designing and building customer and citizen experience platforms that significantly reduce friction in healthcare and government services. His strategies and solutions prioritize enhancing user self-service and transparency through human-centered design, resulting in more intuitive and streamlined interactions. Adam's commitment to reducing fraud, waste, and abuse remains at the forefront of his work, ensuring that systems are not only efficient but also secure and trustworthy. His overarching goal is for CapTech to be the most reliable and effective partner a client could have, driving long-term success and meaningful improvements in service delivery.

Adam Auerbach

Director

Adam is passionate about drawing new insights from health data and building digital experiences that simplify access to meaningful healthcare. Clients rely on his 10+ years of expertise to guide and oversee strategic initiatives ensuring that systems are efficient, scalable, and aligned with stakeholder objectives. A life-long learner and Health Systems Subject Matter Expert (SME), Adam is dedicated to solving complex problems through tech-forward solutions.