Articles October 28, 2021

Consumer-Driven Innovation in 2021

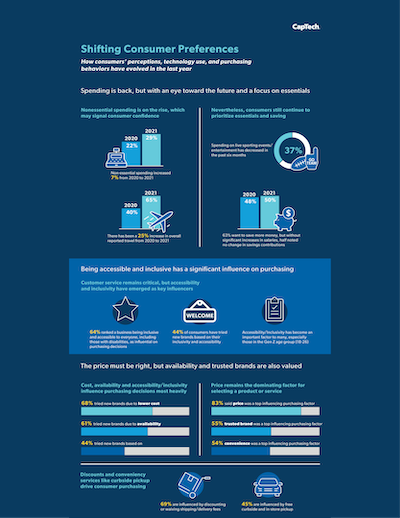

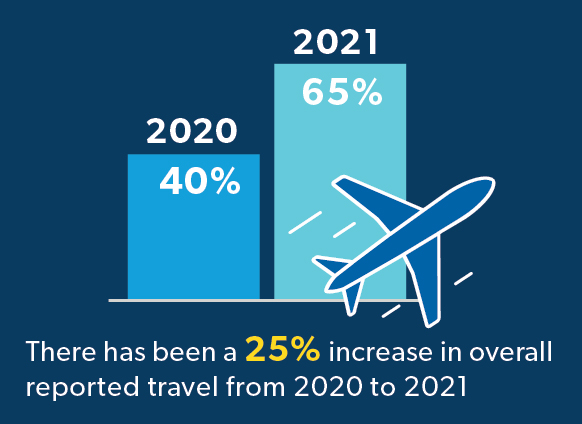

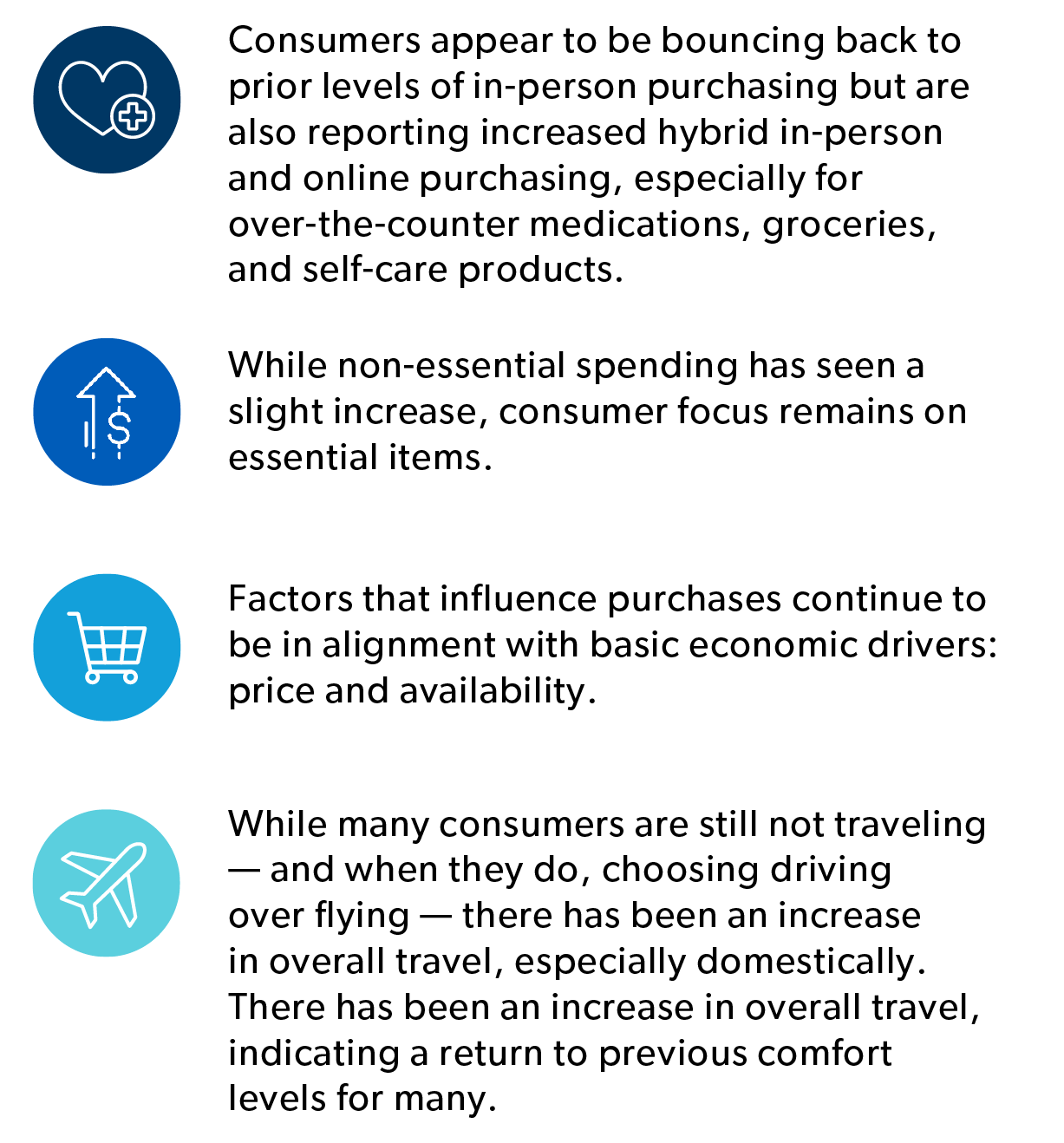

SPENDING IS BACK, BUT WITH AN EYE ON THE FUTURE AND A FOCUS ON ESSENTIALS

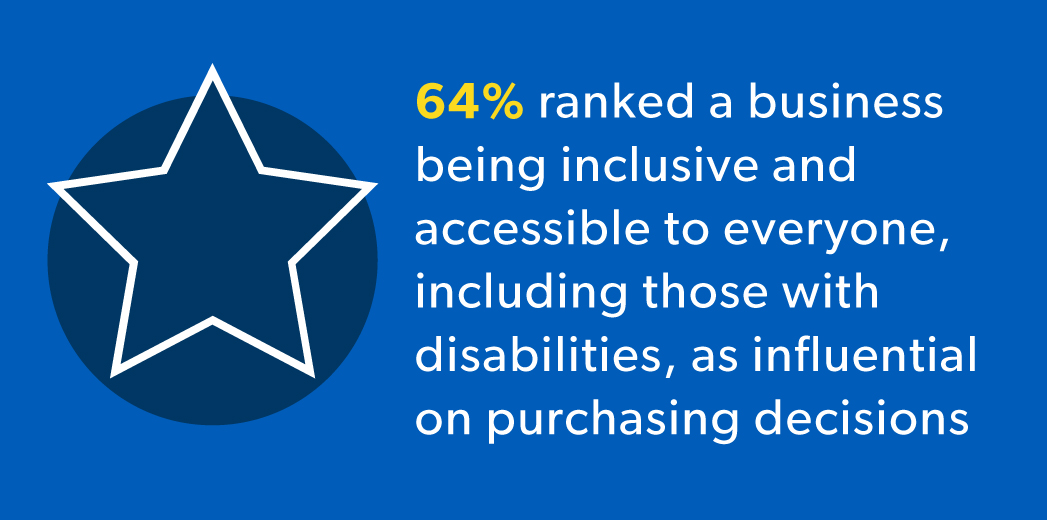

BEING ACCESSIBLE AND INCLUSIVE HAS A SIGNIFICANT INFLUENCE ON PURCHASING

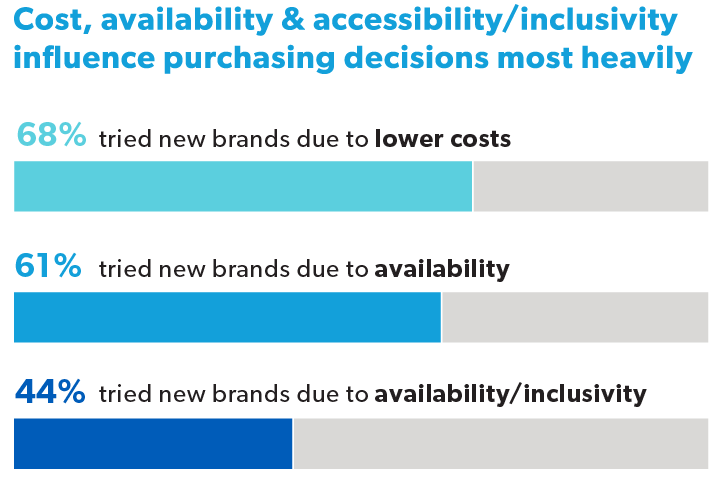

THE PRICE MUST BE RIGHT, BUT AVAILABILITY AND TRUSTED BRANDS ARE ALSO VALUED

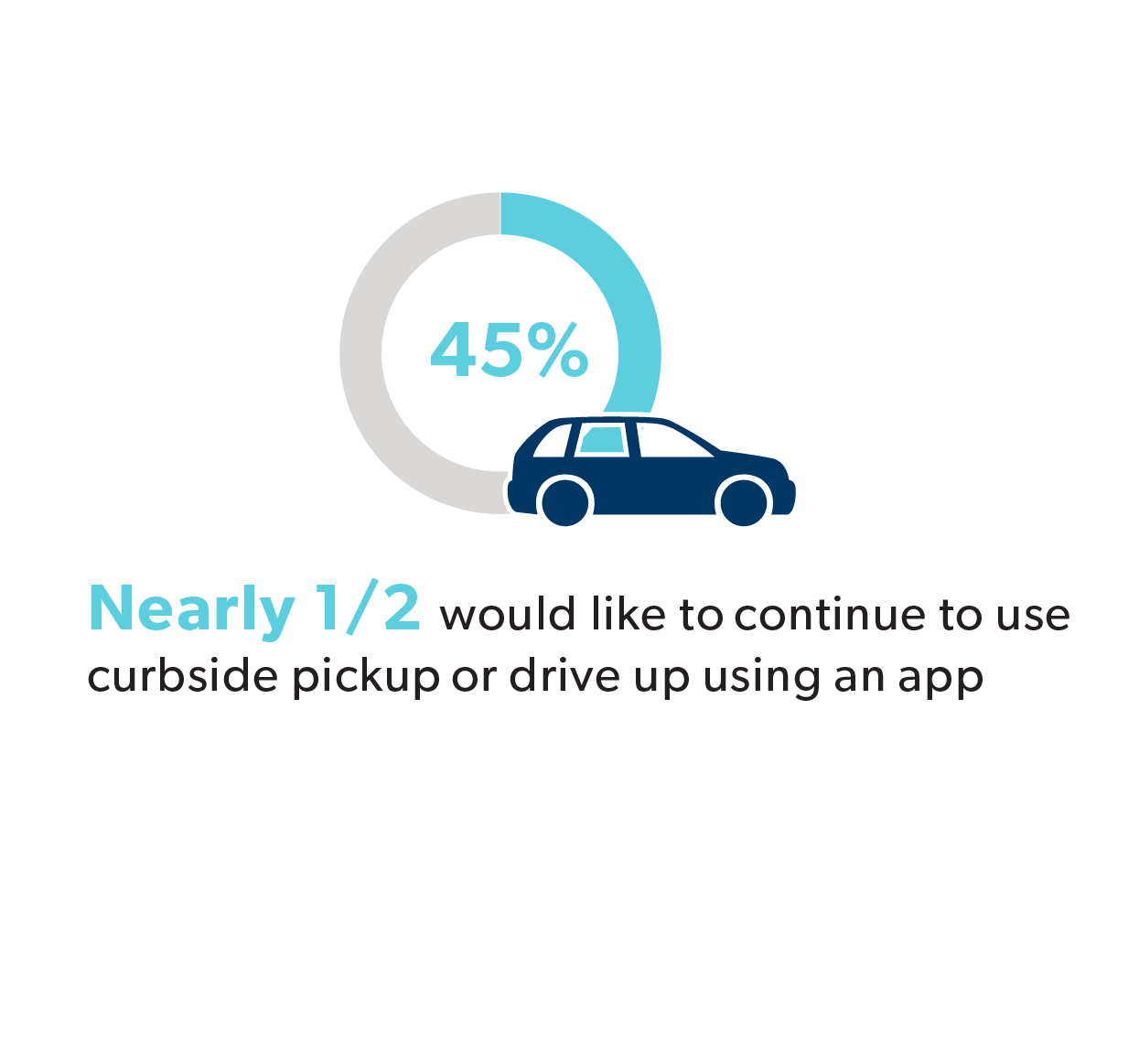

DIGITAL SAVVINESS AND CONSUMPTION ARE HERE TO STAY

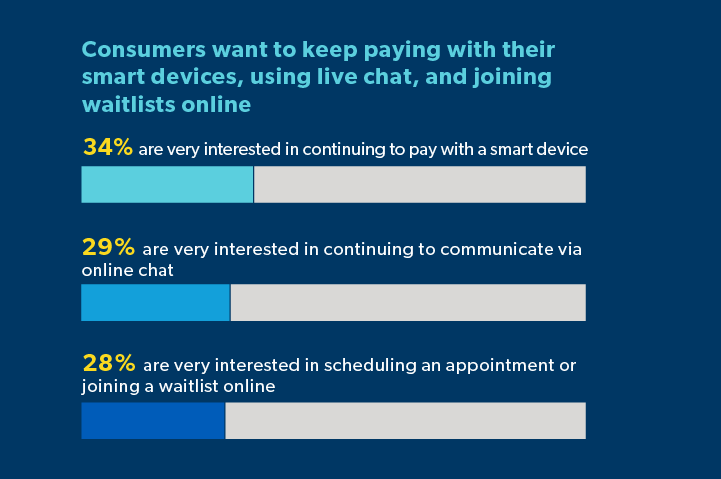

INNOVATIVE TECHNOLOGIES CONTINUE TO MEET CHANGING NEEDS

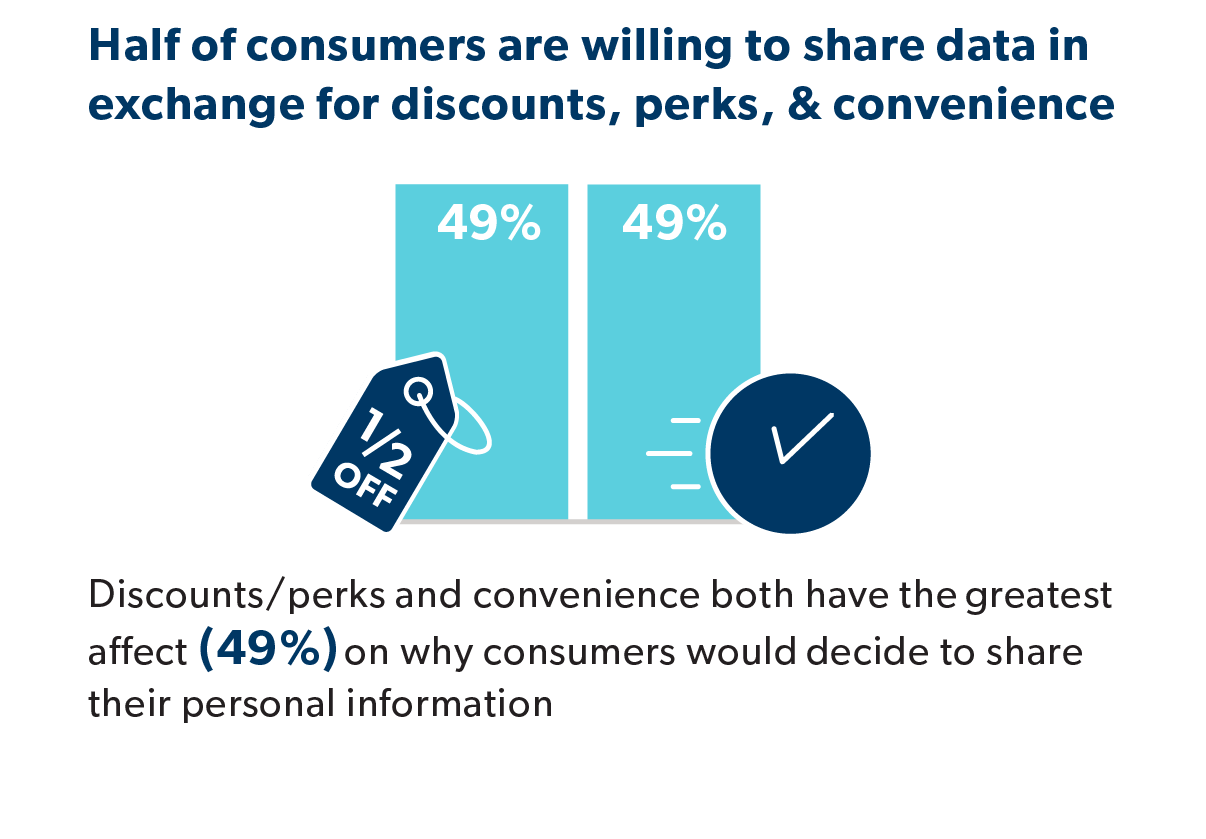

PERSONALIZATION AND CONVENIENCE DRIVE DATA SHARING

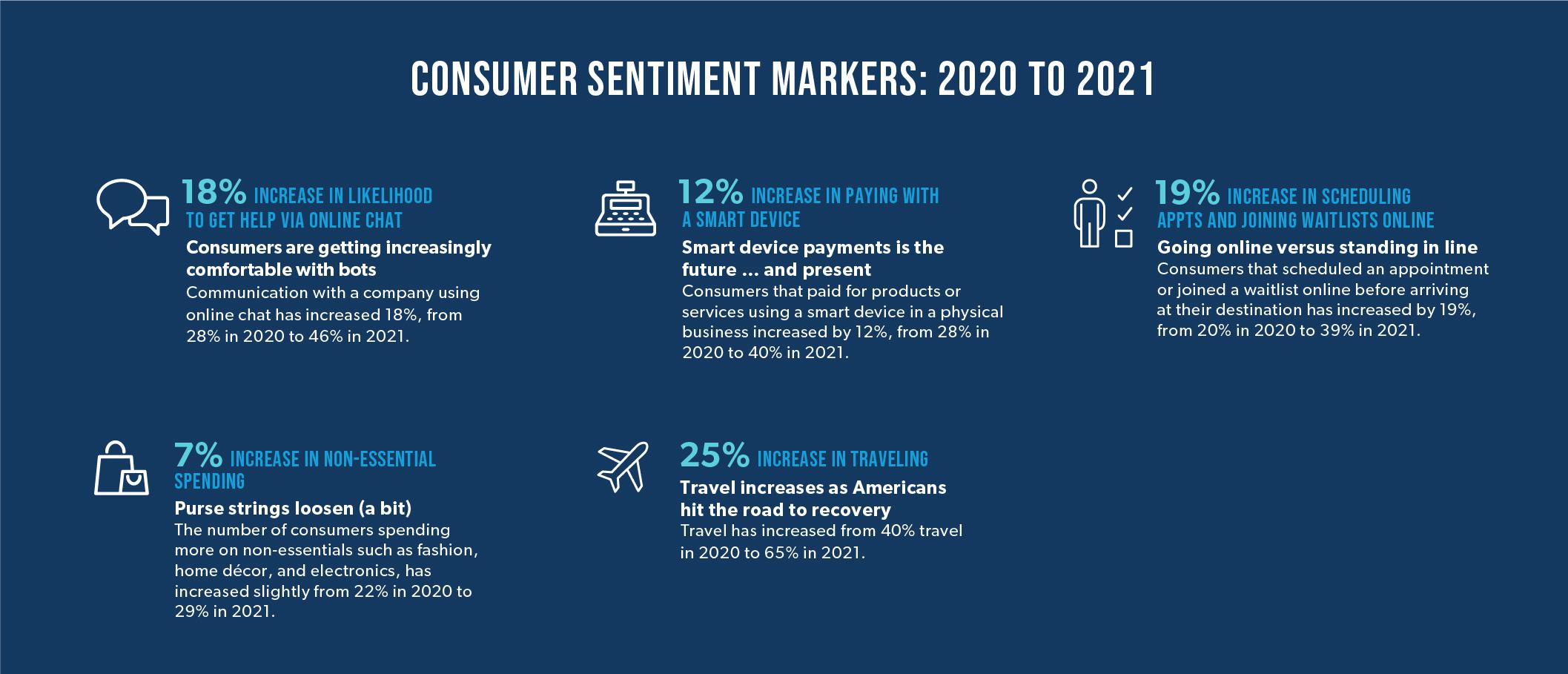

HAS CONSUMER BEHAVIOR RETURNED TO “PRE-COVID-19” NORMS?

THE OPPORTUNITY: KEEPING PACE WITH CONSUMERS

Methodology and Sources

Bree Basham

Principal, CX Practice Area Lead

Bree leads our Customer Experience practice, creating digital strategies and solutions using modern technologies to deliver meaningful and measurable experiences for our customers. She has served as a Creative Director for many omnichannel experiences within the retail space, as well as for a number of other industries that CapTech serves.

Vinnie Schoenfelder

Principal, Strategic Innovation

Vinnie is a Principal at CapTech and plays a large role in helping define services,

forge partnerships, and lead innovation for our clients. As a thought leader, he

regularly helps clients solve their most complex business challenges.